Blog > How Much Does Flood Insurance Cost in Tampa Bay? (2026 Real Numbers)

If you've been reading about flood zones in Tampa Bay and your next thought was "okay, but what will this actually cost me?" ... this post is for you.

Flood insurance is one of the most misunderstood costs in Florida real estate. I've seen buyers overbudget because they assumed the worst, and I've seen buyers get blindsided at closing because they didn't ask early enough.

Here's what I actually see in the field working with buyers across Tampa Bay - from Oldsmar to Clearwater Beach to Harbour Island.

First: Flood Insurance Is Separate From Homeowners Insurance

This surprises a lot of buyers, especially those relocating from the Northeast.

In Florida, flood insurance is its own separate policy. Your standard homeowners insurance does not cover flooding - not from storm surge, not from heavy rain, not from a hurricane.

If you're buying in a high-risk flood zone (AE or VE) with a mortgage, your lender will require a separate flood policy. Budget for both.

What Determines the Cost?

No two flood insurance quotes are the same. Here's what actually moves the number:

Flood zone designation — Zone X, AE, and VE carry very different premiums. More on this below.

Elevation - How high the home sits relative to Base Flood Elevation (BFE) is often the single biggest factor. A home one foot above BFE and a home two feet below BFE on the same street can have wildly different premiums.

Elevation certificate - If the seller has one, get it. It documents the home's exact elevation and can significantly lower your quote. If there isn't one, you can order it — typically $500–$800 — and it often pays for itself in annual savings.

Construction type and age - Newer construction built to post-FIRM (Flood Insurance Rate Map) standards is usually less expensive to insure. Older homes built before flood maps existed can be more expensive. If you're weighing new construction vs. resale, this is one more reason to factor in insurance costs early.

NFIP vs. private flood insurance - You have two main options, and the cheaper one isn't always the obvious one.

NFIP vs. Private Flood Insurance: Which Is Better?

NFIP (National Flood Insurance Program) is the federal program backed by FEMA. It's widely accepted by lenders and offers standardized coverage up to $250,000 for the structure and $100,000 for contents.

Private flood insurance is offered through independent carriers. It can be significantly cheaper in some cases, offer higher coverage limits, and include additional features like loss of use coverage.

Here's what I tell my buyers: get both quotes. The difference can be $1,000 or more per year ... and private carriers are increasingly competitive in the Tampa Bay market.

The catch? Some lenders are more comfortable with NFIP. Always confirm with your lender before switching to a private policy.

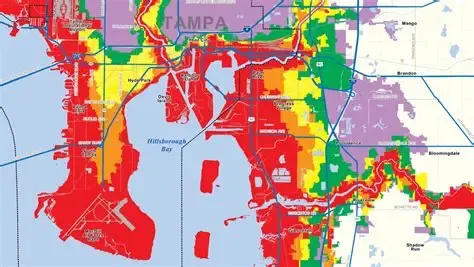

Real Ballpark Numbers by Zone

These are general ranges based on what buyers across Tampa Bay typically see. Your specific quote will depend on the factors above — but this gives you a realistic starting point for budgeting.

Zone X (low-to-moderate risk) Flood insurance is not required by lenders in Zone X, but many buyers still choose to carry it.

- Optional NFIP policy: roughly $400–$900/year

- Many buyers in Oldsmar, Safety Harbor, and inland areas of Palm Harbor fall into Zone X and opt for a low-cost policy for peace of mind

Zone AE (high-risk) This is the most common high-risk zone in Tampa Bay. Required by lenders if you have a mortgage.

- Typical range: $1,500–$5,000+/year depending on elevation and construction

- A well-elevated home above BFE in areas like parts of Shore Acres or Davis Islands can come in on the lower end

- A home below BFE or in a lower-lying area can push significantly higher

- I've seen buyers in Zone AE pay as little as $1,800/year with a strong elevation certificate ... and others pay $4,500+ without one

Zone VE (high-risk coastal) The highest-risk designation ... typically beachfront and open-water properties. Think Clearwater Beach, Madeira Beach, and direct Gulf-front homes.

- Typical range: $4,000–$10,000+/year

- Elevation, construction type, and distance from open water all matter here

- This is where private flood insurance often makes the most sense to shop aggressively

The Condo Exception (This Is Important)

If you're looking at condos — particularly in waterfront communities like Harbour Island, parts of downtown St. Petersburg, or coastal buildings in Clearwater Beach - the flood insurance situation is often very different.

Many Tampa Bay condo associations carry a master flood insurance policy that covers the building structure and common areas. Individual unit owners typically do not need to purchase a separate structural flood policy.

Instead, condo owners usually carry:

- An HO-6 policy (personal property + interior)

- Loss assessment coverage

- Contents coverage

This means a Harbour Island condo in Zone AE might not cost you nearly what a single-family home in the same zone would. Always review the association's insurance documents - your agent (hi, that's me) should pull these for you before you make an offer.

How to Get an Accurate Quote Before You Make an Offer

This is one of the most important things I push my buyers to do - and most don't think to do it until after they're under contract.

Here's what I recommend:

- Identify the flood zone on the FEMA map as soon as you're seriously considering a property

- Request the elevation certificate from the seller if one exists

- Get a flood insurance quote early — ideally before you make an offer, so you know the true cost of ownership

- Compare NFIP and private carriers — ask your insurance agent to run both

- Factor it into your monthly payment — a $3,600/year policy is $300/month added to your budget

I cover this and more in my complete guide on what it costs to buy a home in Tampa Bay ... flood insurance is just one of the line items buyers often don't see coming.

What About Shore Acres, Davis Islands, and Other Known Flood Areas?

These neighborhoods come up a lot because they're desirable - and because buyers hear things about them secondhand.

Shore Acres (St. Pete) - Has a history of flooding and is largely in Zone AE. The city has invested heavily in stormwater infrastructure improvements in recent years. Insurance is required and can be meaningful, but elevation certificates and newer construction make a real difference. Many buyers are comfortable here with the right information. If you're considering the broader St. Pete area, check out what it's like to live in St. Petersburg for the full neighborhood breakdown.

Davis Islands - Mix of Zone X and AE depending on the specific property. Close to water, high lifestyle appeal. Quotes vary widely by block ... two homes a street apart can have very different premiums.

Clearwater Beach - Mix of AE and VE zones. Condo buildings often have master policies. Single-family and townhomes on the beach carry higher premiums but buyers are typically factoring in the lifestyle trade-off. Read our full Clearwater Beach neighborhood overview for more on what to expect there.

Harbour Island — Mostly condo living, so master flood policies are common. One of the reasons buyers find the insurance cost more manageable than expected for a waterfront community. Check our Harbour Island guide for a full breakdown of the lifestyle and costs.

Oldsmar and Safety Harbor — Largely Zone X with pockets of AE near the water. Many buyers in these areas carry optional low-cost policies. Generally very affordable from a flood insurance standpoint. See our Oldsmar overview and Safety Harbor overview for more.

How Does This Fit Into the Bigger Picture?

Flood insurance is one piece of the total cost of owning in Tampa Bay. If you're moving to Tampa Bay in 2026 and building out your budget, make sure you're accounting for:

- Homeowners insurance

- Flood insurance (where applicable)

- HOA fees (very common in Florida — even for single-family homes)

- Property taxes and homestead exemption

- Wind mitigation

Getting all of these numbers early is how you avoid surprises at the closing table.

The Bottom Line

Flood insurance in Tampa Bay is not one-size-fits-all. The zone is just the starting point.

Elevation, construction, certificates, policy type, and whether you're buying a condo or single-family home all affect the final number dramatically.

The buyers who navigate this best are the ones who get a real quote early ... before they fall in love with a house and before they're under contract. That way it's just information, not a surprise.

If you have questions about flood zones or insurance costs for a specific property you're considering, I'm happy to walk through it with you. It's one of the conversations I have almost every week with buyers across Tampa Bay.

👉 Schedule a call with Marianne

And if you haven't read the companion post yet - Everything You Need to Know About Flood Zones in Tampa Bay - that's a great place to start before diving into insurance costs.